Financial results of XTB for 2019

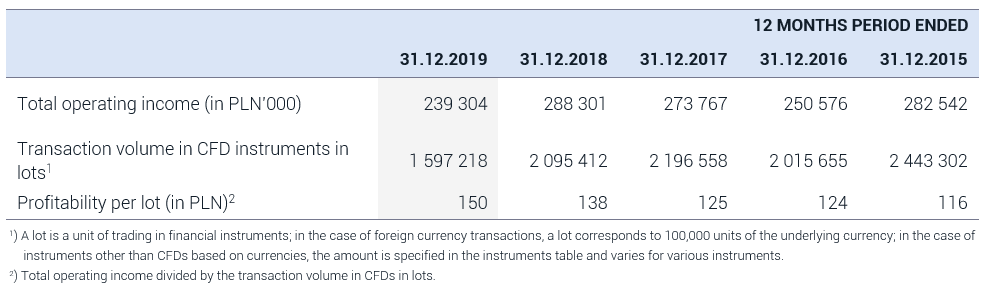

In 2019 XTB reported a consolidated net profit of PLN 57,9 million compared to PLN 101,5 million net profit a year earlier. Consolidated revenues amounted to PLN 239,3 million compared to PLN 288,3 million a year earlier, and operating costs PLN 173,8 million (2018: PLN 172,5 million). The Group gained a record number of new clients, i.e. 36 555, which means an increase by 76,8% y/y.

REVENUES

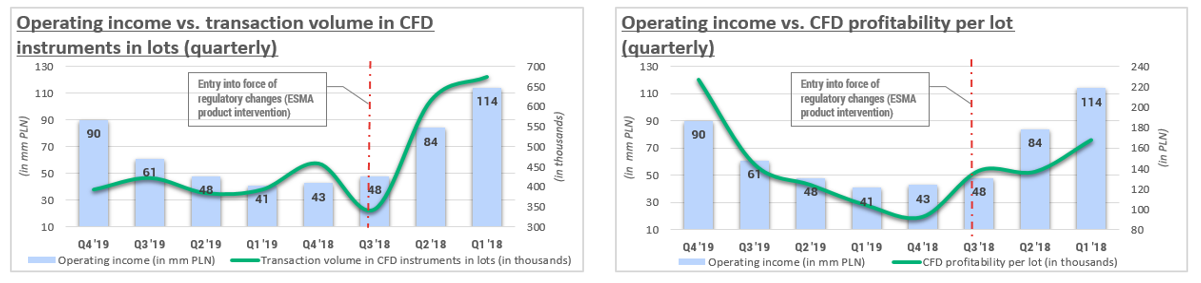

In 2019 the revenues decreased by 17,0 y/y i.e. PLN 48 997 thousand from PLN 288 301 thousand to PLN 239 304 thousand. One of the relevant factors which determined the level of revenues of XTB was the product intervention of ESMA. coming into force in August 2018. The regulations limited maximum permitted level of leverage for retail clients, which resulted in lower volume of transactions concluded by clients. Consequently, CFDs turnover in lots amounted to 1 597 218 lots compared to 2 095 412 a year earlier. Profitability per lot increased by 8,7% y/y i.e. from PLN 138 to PLN 150.

In Q42019, the revenues increased by 109,3% compared to the Q4 2018, i.e. by PLN 46 785 thousand from PLN 42 786 thousand to PLN 89 571 thousand. This change was driven by: (i) higher profitability per lot – an increase by PLN 134 (from PLN 93 to PLN 227); (ii) lower financial instruments turnover noted in the number of concluded transactions in lots – a decrease by 64 723 lots (from 458 869 to 394 147 lots).

XTB has a solid basis for growth in the form of constantly growing customer base and number of active clients. In 2019 the Group reported a record number of new clients amounting to 36 555 compared to 20 672 in 2018, i.e. an increase by 76,8%. This is an effect of continuing the optimized sales and marketing strategy and the successive introduction of new products to the offer, such as CFDs based on sector indices, shares, ETFs and an expansion to new geographical markets. The average number of active clients was higher by 5 303 compared to 2018, i.e. 24,9%. The intention of the Management Board in 2020 is to further increase the client base. This is confirmed by the data for January, when the Group gained a record number of new clients i.e. 4 480.

XTB’s aim is to provide a diversified investment offer simultaneously with comfort of managing the differentiated portfolio on one trading platform. The company analyses other possibilities of expanding the product offer, which could cause the introduction of new products in 2020 and further years.

Looking at revenues in terms of the classes of instruments responsible for their creation, it can be seen that in 2019, CFDs based on stock indices dominated. Their share in the structure of revenues on financial instruments reached 74,8% compared to 49,6% a year earlier. This is a consequence of the high interest of XTB clients in CFD instruments based on the German DAX stock index (DE30) and the US indices US 500 and US 100. The second most-profitable class of assets were CFD based on currencies. Their share in the structure of revenues on financial instruments in 2019 reached 18,2% (2018: 23,5%). Instruments based on the EURUSD currency pair were the most popular among this asset class. The revenues from commodity-based instruments accounted for 5,2% of total revenues, compared to 24,3% a year earlier.

XTB clients, looking for investment opportunities to earn money, generally trade in financial instruments that are characterized by high market volatility in a given period. This may lead to fluctuations in the revenue structure by the asset class, which should be treated as a natural element of the business model. From the point of view of XTB, it is important that the range of financial instruments in the Group’s offer is as broad as possible and allows clients to use every upcoming market opportunity to earn money.

The result of operations on financial instruments

XTB places great importance on the geographical diversification of revenues. The countries from which the Group derives more than 15% of revenues are Poland and Spain with the share of 40,5% (2018: 25,2%) and 19,9% (2018: 14,7%) respectively. The share of other countries in the geographical structure of revenues does not exceed in any case 15%.

XTB also puts strong emphasis on diversification of segment revenues. Therefore the Group develops, besides retail segment, institutional activities (X Open Hub), under which it provides liquidity and technology to other financial institutions, including brokerage houses. Revenues from this segment are subject to significant fluctuations from quarter to quarter, analogically to the retail segment, which is typical for the business model adopted by the Group.

It should be noted that, similar to the retail segment, ESMA product intervention could affect the condition of the European institutional partners of XTB and thus the transaction volume in lots as well as the revenues of XTB from these clients. However, the Management Board cannot exclude that there will been increase in volatility of institutional clients in the future.

OPERATING EXPENSES

Operating expenses in 2019 amounted to PLN 173 892 thousand and were similar to those a year earlier (an increase by PLN 1 400 thousand y/y). The most significant changes y/y occurred in:

• salaries and employee benefits costs, an increase by PLN 7 546 thousand mainly due to new employment and employee

severance payments;

• marketing costs, an increase by PLN 4 394 thousand mainly due to higher expenditures on online marketing campaigns;

• costs of maintenance and lease of buildings, a decrease by PLN 4 657 and consequently an increase in depreciation costs by

PLN 2 822, relating to the entry into force of IFRS 16 Leasing;

• other costs, a decrease by PLN 9 746 thousand as a result of one-off event in Q3 2018 in the amount of PLN 9 900 thousand.

The Management Board expects that in 2020 operating expenses should be at a level of several percent higher than in 2019. The final level will depend on the pace of geographical expansion into new markets, the variable remuneration elements (bonuses) paid to employees, the level of marketing expenditures and the impact of regulations and other external factors on the level of revenues generated by the Group.

DEVELOPMENT PERSPECTIVES

- The entry into force of product intervention by ESMA creates both opportunities and threats for XTB. On the one hand, there is a temporary drop in trade volumes among European brokers. On the other hand, the Management Board of XTB is convinced of the business’s vitality over a longer time horizon. The natural consequence of ESMA’s decision should be a wave of consolidation on the market that would allow XTB to consolidate its strong position on the European market. Less influential brokers, unable to withstand regulatory pressure and strong competition from a very significant brokers, will naturally disappear from the market. Consequently large brokers should expect the client base to grow.

XTB with its strong market position and dynamically growing client base enters the non-European markets. XTB is consequently implementing a strategy on building a global brand. The Group aims to increase its European market penetration and continue with building their position in Latin America, Asia and Africa.