XTB financial results for the 1st half of 2017

In the I half of 2017 consolidated operating profit (EBIT) increased by PLN 34.1 million, i.e. 183.0%, and reached PLN 52.7 million in comparison to PLN 18.6 million as compared to the same period of the previous year. Net profit was PLN 29.4 million, compared to PLN 23.0 million in a previous year. That’s an increase of 27.8%.

The net result for the I half of 2017 was mainly shaped by the following factors:

- 183,0% increase in operating result (EBIT) due to:

a. the increase of 10.0% in operating income due to higher profitability per lot;

b. improved cost-effectiveness, showing a decrease by PLN 22.7 million in operating costs; - factors not related to core operational activities, ie:

a. creation of impairment write-down of separate intangible assets in the form of a brokerage license in the Turkish market in amount of PLN 5.6 million;

b. occurrence of negative exchange rate differences (finance costs) in the amount of PLN 12.2 million (I half of 2016: PLN 2.9 million) as a result of zloty strengthening against other currencies.

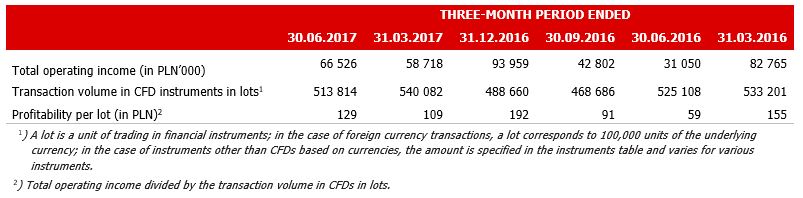

Operating revenues increased by 10.0% and reached PLN 125.2 million in the I half of 2017 in comparison to PLN 113.8 million as compared to the previous year. From the structural side they have been shaped by an increase in profitability per lot with a comparable volume of transaction in CFD instruments in lots.

The XTB has a stable foundation for future growth in the form of a growing customer base. In the II quarter of 2017, the number of new accounts was the same as in the IV quarter of 2016, while in the I quarter of this year The Group reached the record number of new accounts. The total number of new accounts in the I half of 2017 increased by 68.3% over the comparable period. The average number of active accounts in the first half of 2017 amounted to 20 016, an increase by 22.8% y/y.

According to the Management Board, in the coming months a significant portion of XTB branches should maintain the increasing rate number of accounts that observed in 2017. Germany, France and Latin America have the biggest potential for business growth. Increasing accounts is not only the result of an optimized sales and marketing strategy, but also the result of product and technology development. The management continues to see great potential in technology and product development, which should help XTB expand its customer base and reach customers who have not previously been the Group’s main target customers.

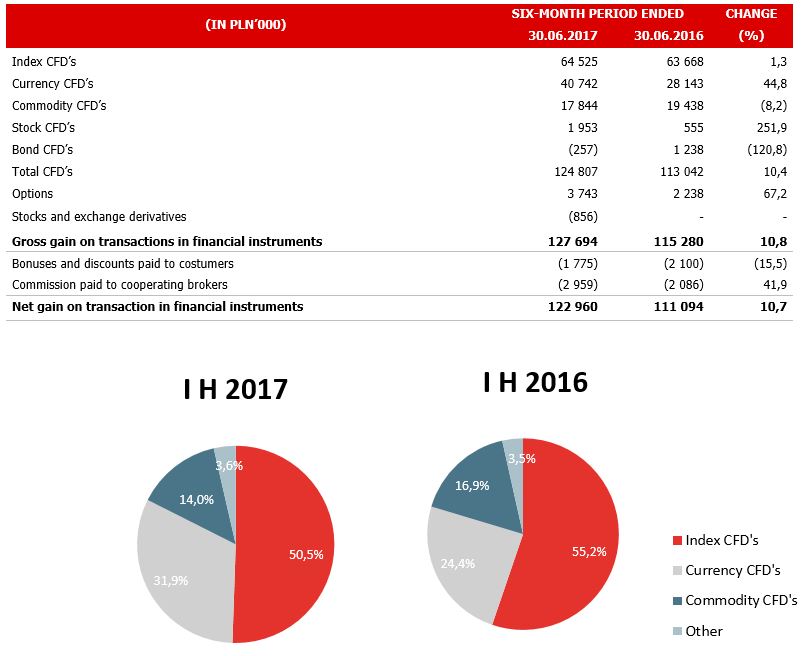

Looking at the revenue structure for the classes of instruments responsible for their origins, we see that more than half of revenue was generated on CFDs based on stock indices. The most important of these are CFD based on German and American stock indices (DE30, US500, US100, US30). Looking at the structure in greater detail, it can be seen that the increase in revenues is primarily attributable to CFDs on currencies.

Geographically, XTB revenues were well diversified. Their growth has occurred in both Central and Eastern Europe and Western Europe. Countries where the Group derives more than 15% of its revenues each are: Spain (23.0%, decrease of share from 25.5%) and Poland (19.4%, decrease of share from 23.4%). The share of other countries in the geographic structure of revenues does not exceed in any case 15%. Latin America is also gaining on global relevance.

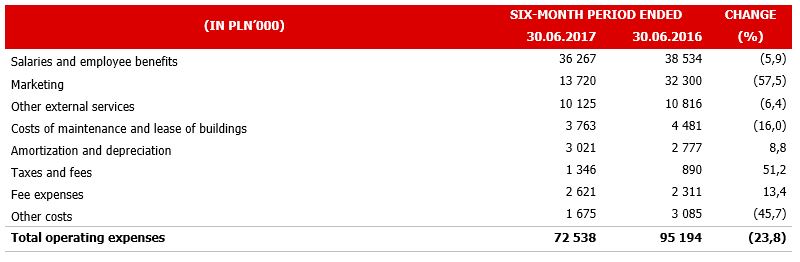

In the I half of 2017, XTB managed to significantly improve cost-effectiveness compared to the same period of the previous year, while maintaining growth in number of new accounts and number of active accounts. Operating expenses in the first half of 2017 amounted to PLN 72.5 million, a decrease by 23.8% y/y. This decrease was attributed to the lower by PLN 18.6 million y/y in marketing costs, mainly due to lower spending on advertising campaigns.

The Management Board expects that in the II half of 2017 operating costs should be at a level comparable to that of the I half of 2017. The final level of operating expenses will depend on the variable remuneration components paid to employees and the level of marketing expenditure. The amount of variable remuneration components will influence the results of the Group. The level of marketing expenditures will depend of their impact on the performance and profitability of the Group and on the responsiveness of customers to the actions taken.

Take a decision on the Turkish subsidiary X Trade Brokers Menkul Değerler A.Ş. (Current report no. 15/2017) required the establishment of a write-down of the value of a separate intangible asset in the consolidated financial statements for the I half of 2017 in the form of a brokerage license for the Turkish market of approx. PLN 5.6 million.

The XTB Group operates in the international markets, whereby it owns cash in different currencies. This results in foreign exchange, positive and negative exchange rates occurring during the reporting periods. Due to significant zloty appreciation in the I half of 2017, the Group recorded negative exchange differences (financial expenses) in the amount of PLN 12.2 million (I half of 2016: PLN 2.9 million).

The current regulatory changes in the industry at national and international level may change its face in the long run. On the one hand, the European Securities and Markets Authority (ESMA) published on 29 June this year statement regarding possible product interventions for CFDs, binary options and other highly speculative financial products that would take place under MIFIR. In a statement, ESMA informed that Limiting the level of leverage, banning the offering of bonuses, introducing the protection against negative balance and restrictions on advertising and promotion. According to ESMA, the product interval would enter into force at the earliest January 3, 2018. On the other hand, in Poland in July this year, The draft amendment to the Act on the Amendment to the Financial Market Supervision Act and a number of other statutes has been published to show that the government is planning to reduce the maximum leverage to 1:25 for FX / CFD investors.

The proposed restrictions on the FX/CFD market are aimed at protecting retail investors primarily against market abuse, which undermined trust in the entire securities and securities industry. In the opinion of the Company, as regards the Polish market from which the Group currently achieves 19.4% of its revenues, it will be crucial to ensure uniform operating conditions for all market participants so that legislative actions do not harm Polish investors by supporting the development of the grey market of foreign entities, where the domestic investor will look for products that are optimal for his investment portfolio. Introducing the proposed one-sided restrictions for the domestic FX/CFD industry while neglecting the actions of foreign entities will be detrimental to the Polish client and the entire market. It should be noted that we are currently dealing with a project, which is not clear with the mere adoption of the changes in the shape presented in it. The legacy of our parliamentary legislative experience (e.g. with regard to the final determination of MAR sanctions) shows that, as part of the work on the project, it has undergone another change, evolving to a final version that has not always been concise and accurate. With the originally announced project. At this moment it is therefore not at all determined that the proposed changes will be enacted and will become effective.

The above-described market environment is for XTB as an internationally traded entity with a well-diversified geographical revenue base and stable operating fundamentals, an opportunity to consolidate the industry at national and international level. The XTB board sees one of the Group’s development directions.

In addition, the Company’s current management plans for the forthcoming periods assume accelerated development of the Group, in particular by expanding the client base, further penetrating existing markets, and accelerating geographical expansion into Latin American markets.